In his article for Soaked by Slush, Christian Owens, co-founder and CEO of the scaleup Paddle raises the concern that the metrics currently used to quantify European tech success are due for a change. The overemphasis on unicorns leads to a tunnel vision in which only the gigantic exits are valued, and the numerous smaller ones neglected. The author argues that the overall health of the European startup ecosystem rests on the hundreds and thousands of small businesses becoming successful and scaling up only when solid foundations are built, instead of seeking aggressive growth via big funding rounds.

Our team at Gorilla Capital fully endorses this view. In our opinion, start-ups often try to jump the growth curve, and end up trying to scale a product which hasn’t yet had time to morph into its final version. This behaviour is often due to the phenomenon mentioned above. If a billion-euro valuation is seen as the holy grail, many companies adopt a mindset of aggressive early-stage growth without taking the time to ponder whether their product is ready to be scaled.

That is why we actually seek “camels” instead of unicorns. These are the companies that are capital efficient, have solid unit economics, and focus on building sustainable growth. Admittedly, the initial growth rate may be slower than that of an aspiring unicorn, but these companies are more robust and resilient than their peers.

In good times, the camels thrive, but even under uncertainty, they survive, unlike the aspiring unicorns that jumped the growth curve with high valuations and wind up with downs rounds when the overall economic climate worsens and the bubble bursts.

Stop talking about unicorns: The way we measure European tech success needs to change:

Stop talking about unicorns: The way we measure European tech success needs to change: https://www.slush.org/article/stop-talking-about-unicorns-european-techsuccess-needs-change/

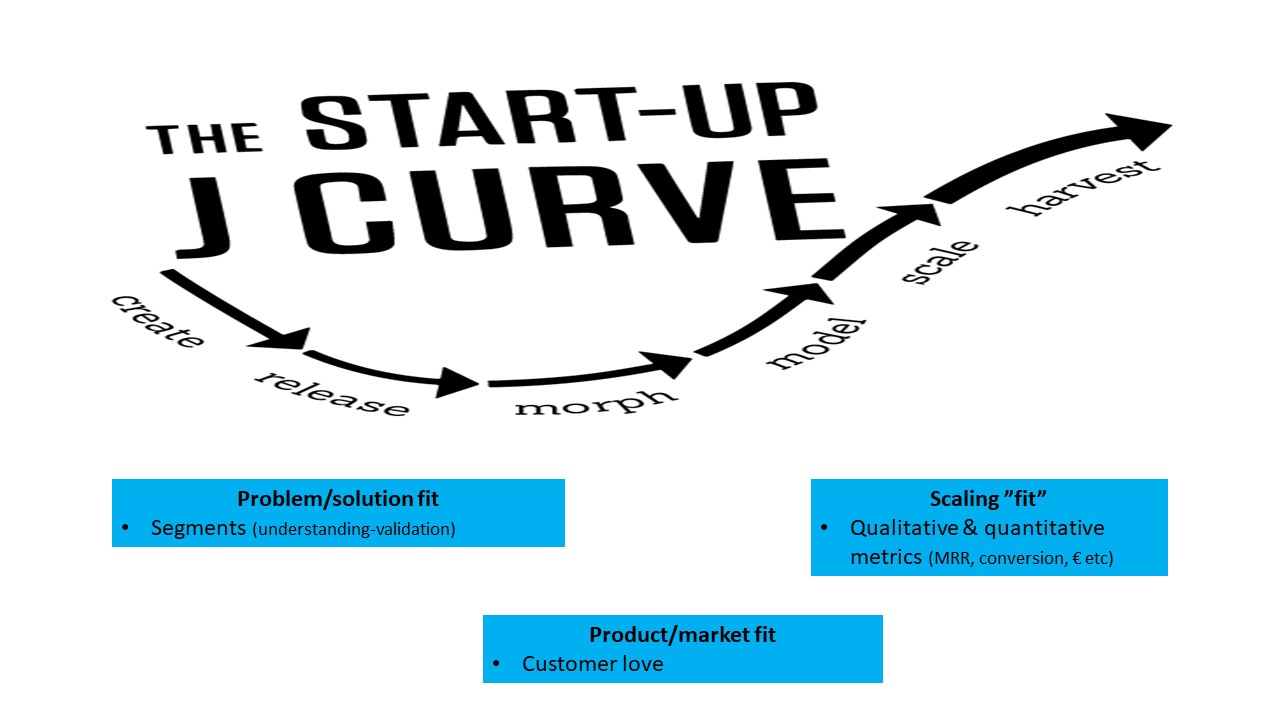

Startups have different stages. Howard Love has well articulated the different stages and we have included the problem/solution fit, product/market fit and scaling “fit” for you to understand how these stages overlap each other.

Where is your startup ? What are the KPI’s relevant for the stage you are in ? Have you “overleaped” one of the stages ? What kind of verification and facts do you have ?

Please note that what gets the media attention are the odd exceptions, not the median cases – as the median cases are boring. Many entrepreneurs dream about an exit - in reality exits (any kind, even small) are rare and on average much smaller than people usually think. Only a part of exits are disclosed (ie. amount becomes public, latest at buyer’s annual report) and as a rule, non-disclosed exits are smaller (typically <10m€) than the disclosed ones. In Nordics a median for a disclosed exit for a technology company is 12-15m€ , for non-disclosed less than that. Typical US technology exit is estimated to be around 5m$.

Whatever both parties accept is OK, there is no book value. As to us, we compare the suggested valuation primarily against what has been achieved to date, secondarily to what the plan is “promising”. The higher the price tag, the more you are expected to have already, and the more is expected from you going forward. And while there is no “List” price, professional investors know what kind of companies have been able to close rounds at what valuations, which gives a comparable. Worth noting is that any founder with experience in fundraising will tell you that more important than the valuation, or even the amount raised, is that the process is quick and smooth, allowing you to get back to doing business as soon as possible. If you try something that is unrealistic, you will learn the hard way the wisdom behind that.